When Donald J. Trump championed the idea of a 10 percent blanket tariff during the campaign, many people, whether for or against, were taken aback by how radical the idea was.

Alarms sounded about higher inflation, lost jobs, slower growth or recession. The prospect seemed so outlandish that most economists and Wall Street analysts who gamed out the possibilities tended to treat a 10 percent tariff simply as a bargaining tool.

Now, after a rapid-fire series of announcements from the White House that promised, imposed, reversed, delayed, decreased and increased tariffs, the 10 percent solution is looking like the most temperate choice rather than the most revolutionary, especially now that a red-hot trade war between China and the United States is blazing.

Yet 10 percent tariffs have not lost their sting.

At that level, universal tariffs still hit more than 10 times as many imports as the ones targeted during Mr. Trump’s first term, and are significantly higher and broader than anything the United States has tried in more than 90 years.

The tariff rate is “quite extreme,” said Carsten Brzeski, chief eurozone economist at ING, a Dutch bank. “It still brings us back to levels last seen during the 1930s.”

In addition to measures targeting China, Mr. Trump powered up a long list of punishing taxes — including a flat 10 percent tariff on most imports — on April 9.

“For the U.S. customer, it means everything is going to become more expensive,” Mr. Brzeski said.

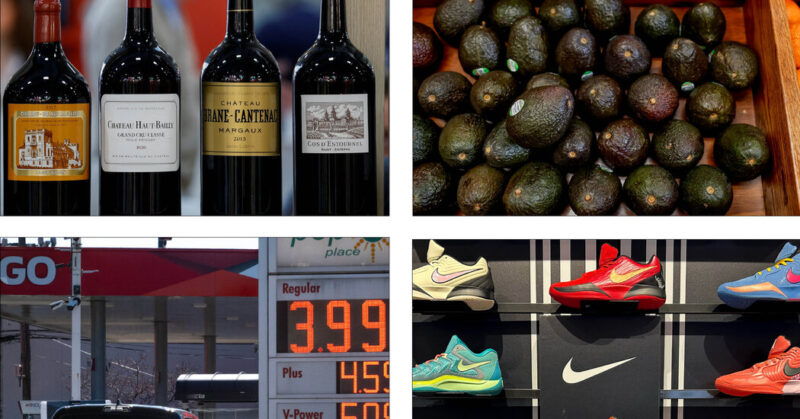

Researchers have previously estimated that a 10 percent tariff would cost the average American household $1,700 to $2,350 more a year.

Switching to, say, a cheaper American brand of mustard instead of a French one may save a shopper less than hoped. When tariffs on a foreign good go up, domestic manufacturers can take the opportunity to raise their own prices, economists have found.

What are tariffs, and why might they cause prices to go up? Here is an explainer from The New York Times:

A tariff is a government surcharge on products imported from other countries.

Tariffs are paid by the companies that import the goods. The revenue from U.S. tariffs is paid by U.S. importers to the U.S. Treasury Department.

For example, if Walmart imports a $100 shoe from Vietnam — which faces a 46 percent tariff — Walmart will owe $46.00 in tariffs to the U.S. government.

What happens next?

Walmart could try to force the cost onto the Vietnamese shoe manufacturer, by telling it Walmart will pay less for the product.

Walmart could cut into its own profit margins and absorb the cost of the tariff.

Walmart could raise the price of the shoes at its stores.

Or, some combination of the above.

Economists found that, when Mr. Trump put tariffs on China in his first term, most of that cost was passed on to consumers. But economic studies found that his tariffs on foreign steel were a bit different; only about half of those costs were passed on to customers.

How much do you and your family talk about money? What are those conversations typically like? Have you been talking about the economy recently — about tariffs, the stock market, your parents’ jobs or businesses or anything else?

Has the economic upheaval of the past week affected how you and your family are handling money? Are you pulling back on your spending? Stocking up on items that might get more expensive? Investing in the stock market? Or are you operating as usual?

Caitlin McGarry writes in Wirecutter, “Nearly anything you buy is likely to be affected by tariffs in some way.” If prices do increase for items like electronics, clothing or food, how might that change your shopping habits?

What is your reaction to Mr. Trump’s tariffs? Do you think they are an important tool for addressing imbalances in international trade and providing tax revenue for the American government, as the economist Oren Cass suggests? Or will the White House’s haphazard rollout ultimately be ineffective and damage the American people and economy, as the Times Editorial Board argues?

Financial anxiety among Americans has been running high for years, according to a recent article on the topic. “Since Covid, we’ve all just been waiting for the next shoe to drop, moneywise,” Megan McCoy, a financial therapist, told The Times. Does that ring true to you? Have you and your family felt on edge about money or the economy in recent years? Why or why not?

The Times has offered advice for coping with the current economic uncertainty. A money columnist, for example, warns not to panic-buy, and a personal tech columnist suggests ways to make your electronics last. What is some wise advice you have received about money, especially when you’re worried about it? How might you apply it to this moment?

{kind=link}